by Datuk Stewart Labrooy

In the Malaysian capital market landscape, few instruments have been as quietly successful as the Real Estate Investment Trust (REIT). Over two decades, M-REITs have evolved from a niche product into a RM55bil bellwether of institutional stability, offering retirees a rare combination of liquidity, transparency and predictable yield.

Central to this success has been the withholding tax exemption on distributed income. Policymakers often frame this as a concession - a generous tax break. This framing is dangerously shortsighted. In reality, this exemption is a structural cornerstone of a functioning REIT regime and applied globally. To remove it would unravel the very contract that built the industry.

Crucially, recent analyst reports confirm that this change does not affect REITs' own earnings, cash flow or operations. The trust-level tax exemption under Section 61A of the Income Tax Act 1967 remains intact. The issue is entirely an investor-side one.

However, this distinction misses the point. The stability of the REIT market depends on the behaviour of its investors, and more importantly, global fund managers. When the after-tax return to capital is reduced or made uncertain, capital flows elsewhere.

A policy that defeats its purpose

What is remarkable about this policy shift is that it will likely reduce the very tax revenue it purports to protect. For a typical retiree investor holding RM1.98mil in REITs with a 6% yield, the financial breakdown is remarkably efficient. At this level, the portfolio generates an annual distribution of RM119,004.

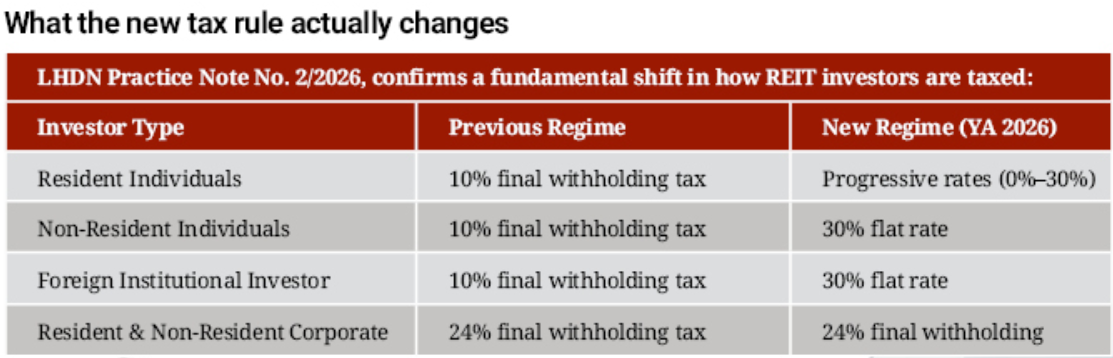

Under Malaysia’s current tax structure, the progressive tax payable on this income would amount to RM11,901. Interestingly, this nearly mirrors the RM11,900 that would be incurred if the same distribution were subject to a flat 10% Withholding Tax (WHT), illustrating a balanced tax impact for high-value retail investors (see table).

The result is virtually identical. But the vast majority of individual investors hold far less than RM2mil. For these investors, the progressive tax system will yield substantially less revenue than the flat 10% withholding tax.

Therefore, the new tax regime will result in the following:

· Collection of less tax from the majority of retail investors

· Incur higher administrative costs (monitoring thousands of individual taxpayers instead of collecting from 19 REIT managers)

· Create complexity for retirees who must now accurately compile annual distributions and calculate tax payable

· Invite legal challenges from investors who may claim distributions constitute rental income, allowing deductions for borrowing costs and other expenses

This is fiscal inefficiency dressed up as reform.

A deeper problem

While recent analyst reports note that yields remain attractive at 4.7% to 6.0%, and that the sector is supported by healthy occupancy rates, rental reversions and acquisition pipelines, these reports are built on the assumption of a stable investor base. That assumption is now in question.

1. The collapse of the yield proposition

M-REITs have historically traded at yields that absorb market volatility. If progressive tax rates apply to distributions, net yield becomes uncertain and, especially for higher-income investors, significantly reduced. A product that once provided inflation-beating, passive income would lose its appeal to precisely the demographic, retirees and income-focused investors that capital market inclusivity aims to serve.

2. Capital flight and liquidity drain

The institutional backbone of M-REITs consists of pension funds, insurers and foreign institutions. If post-tax returns fall below comparable regional markets (Singapore, Australia which maintain clear transparency regimes), these allocators will reallocate cross-border.

Analysts describe this as a near-term repricing and capital rotation. But capital that rotates out rarely rotates back. The liquidity of the local bourse would suffer. More critically, the ability of REITs to conduct acquisitions which relies on equity fundraising and debt servicing would be impaired. A REIT that cannot raise capital cannot grow.

The unintended consequences

The multiplier effect is often ignored. The M-REIT industry is a significant custodian of commercial real estate. By providing a liquid exit mechanism for developers, REITs recycle capital back into the construction sector. If the REIT market falters due to unattractive yields, the entire property ecosystem suffers. Developers lose their most efficient exit mechanism and banks face increased exposure to illiquid commercial assets.

Furthermore, the government would likely experience a net negative fiscal impact. While they might theoretically collect income tax from individuals, they would lose substantial revenue from:

· Stamp duty on asset transactions that cease

· Real Property Gains Tax on stagnant assets

· Corporate tax from developers who can no longer recycle assets

· Income tax from investors who shift capital offshore

A rare alignment of views

Analysts remain overweight on the sector, citing strong fundamentals. But their optimism rests on a fragile premise, that a change to investor-side taxation will not alter investor behaviour.

The current system, a clean, predictable 10% withholding tax collected at source, has operated without complaint for years. It provides LHDN with a steady, timely stream of tax revenue, requires minimal administrative oversight and offers investors certainty of outcome. Replacing this with self-declaration, progressive rates and potential disputes is a step backwards.

The withholding tax exemption is not a gift to the rich; it is the structural lynchpin of a democratized property investment model. To remove it is to misunderstand both the architecture of the asset class and the practical realities of tax administration.

What we have now is a situation which will result in lower tax collection with higher costs incurred, possible legal uncertainty and no meaningful fiscal benefit, all while destabilising an RM55bil industry that supports retirees, developers and the broader property market. Analysts note that fundamentals remain strong. But strong fundamentals cannot withstand a policy that systematically disincentives the very capital that makes those fundamentals possible.

For the sake of Malaysia's capital market maturity, the financial security of retirees and the efficient administration of our tax system, the withholding tax regime must be preserved, not as a concession but as the non-negotiable foundation of a dynamic REIT industry.

executive chairman of AREA Group

of Companies.

This article was first published in StarBiz 7.

Stay ahead of the crowd and enjoy fresh insights on real estate, property development and lifestyle trends when you subscribe to our newsletter and follow us on social media.