Strategic moves to slash mortgage repayments

By Joseph Wong

Unlike savvy investors, many first-time home buyers fall into the trap of paying more than they should when they sign the Sales and Purchase Agreement. Few stop to consider their options and fewer ask this question: How can I stop paying the bank and start owning my home faster?

A staggering number of first-time home buyers tend to stretch out their mortgage to the standard 30-year term, attracted by the offer of lower monthly installments, even if they could afford to pay a little more. What most fail to see is the hidden cost, which is the staggering amount of interest accrued over three decades.

The power of term compression

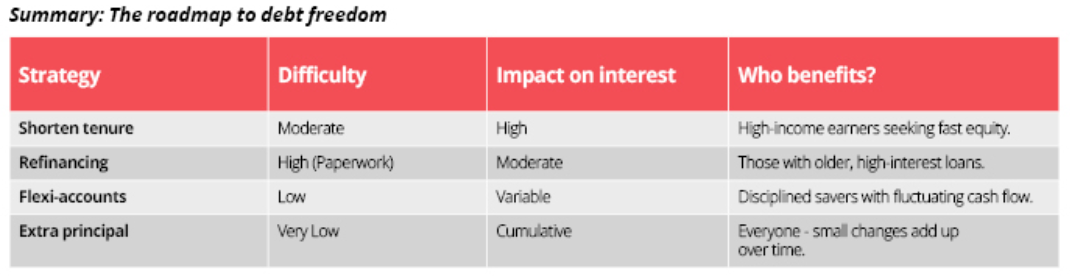

The most straightforward way to save on interest is to opt for a shorter loan tenure. While a 30-year loan is the default for many young buyers due to lower monthly commitments, it is often an interest trap.

Imagine a loan of RM500,000 at an interest rate of 4.5%.

- 30-year term: The monthly repayment is approximately RM2,533. Total interest paid over the life of the loan? RM412,034.

- 20-year term: The monthly repayment rises to RM3,163. However, the total interest paid drops to RM259,186.

By paying an extra RM630 per month, buyers save RM152,848 in interest and own their home a full decade sooner. Of course, not everyone can afford to pay substantially more if their salary cannot sustain the higher monthly repayment. The trick is to calculate what is an acceptable level. Banks can package home loans to suit the buyer, even if the duration of the term is an odd figure. A word of caution: Make sure to leave enough leeway for fluctuating interest rates.

Strategic refinancing: Timing the market

Refinancing involves replacing a current mortgage with a new one, typically to take advantage of lower interest rates or better loan terms. In 2026, with the emergence of Green Mortgages (loans with lower rates for energy-efficient homes), refinancing has become a popular tool for value creation. When to refinance:

- Rate drops: If current market rates are at least 1% lower than the existing rate.

- Improved credit score: If the owners’ buyer eligibility has improved (better DSR or CCRIS), they can negotiate a prime rate that wasn't available to them years ago.

- Switching loan types: Moving from a fixed rate to a flexi-Loan can be beneficial if borrowers now have more disposable income to park into their current account.

Pro Tip: Always calculate the break-even point. Refinancing involves legal fees, valuation fees and stamp duty. If it takes three years of savings to cover these costs and the owner plans to sell in two years, refinancing is a losing move.

Leveraging on flexi and semi-flexi loans

In Malaysia, most modern mortgages are semi-flexi or full-flexi. These accounts are linked to a current account. Every ringgit keep in that linked account acts as a buffer that reduces the principal amount on which interest is calculated.

- How it works: If you have a RM400,000 loan and you park RM50,000 in your linked flexi-account, the bank only charges interest on RM350,000.

- The strategy: Use this account for your emergency savings or bonuses. Even keeping your salary in there for two weeks before paying bills can slightly reduce the daily-calculated interest.

The bi-weekly or extra principal payment

There is no need for a new contract to save money. Most banks allow borrowers to make extra capital repayments.

- Rounding up: If your installment is RM2,533, pay RM2,700. That extra RM167 goes directly toward the principal.

- The 13th month strategy: Making one extra full monthly payment per year can shave roughly 4 to 5 years off a 30-year mortgage.

Negotiating with the bank

Before looking elsewhere for refinancing, talk to your existing bank. This is known as repricing. Banks are often willing to lower your rate slightly to prevent you from moving to a competitor (which costs them a customer). Inform the bank that you are considering a move to a star-performing developer-linked bank scheme and they may offer a retention rate that saves you the legal hassle of a full refinance.

Reducing any mortgage is like running a marathon, not a sprint. By combining a shorter term with the discipline of extra principal payments, borrowers can effectively beat the bank. In the property market of 2026, the true value creation isn't just in the house price but in the interest you don't pay.

Stay ahead of the crowd and enjoy fresh insights on real estate, property development and lifestyle trends when you subscribe to our newsletter and follow us on social media.