Such loans are posing significant risks to banks, regulators and homebuyers

By Joseph Wong

In Malaysia’s property market, the troubling practice of mark-up loans has quietly crept in over the years, creating significant risks for banks, regulators and genuine homebuyers. Although clearly illegal, the issue remains prevalent, driven by complex market dynamics and systemic vulnerabilities. Understanding the persistence of mark-up loans can illuminate effective strategies to combat this fraudulent financing.

A mark-up loan occurs when a property’s valuation is artificially inflated to secure a higher loan amount than the property’s actual market value justifies. Often, this inflated valuation is facilitated through collusion among buyers, sellers, agents and occasionally valuation professionals. This deceptive practice typically results in excess funds, misleadingly promoted as cashback, enticing buyers with additional liquidity sometimes, to cover the cost of the downpayment, renovation or repayment of debt.

What many may be unaware is that the parties to the transaction may be punishable for the offence of cheating, fraud or abetment under the Penal Code (Act 574) if they are proven to be guilty.

“Such fraudulent activities violate banking regulations and ethical standards, constituting financial fraud by misleading lending institutions. However, despite stringent regulations and penalties, mark-up loans persist due to deeper systemic issues in the property financing ecosystem,” observed PEPS Ventures Bhd board advisor Joe Hock Thor.

Several market forces encourage buyers to pursue mark-up loans which include:

Affordability pressures - Rapidly increasing property prices relative to incomes compel prospective buyers to seek risky financing alternatives.

Speculative activities - Investors often engage in property flipping, using inflated loans to minimise upfront capital outlay.

Additional liquidity - The prospect of extra cash labeled as cashback is attractive to buyers who wish to use the additional funds for renovations or speculative investments.

Unethical advice - Buyers may receive misguided financial advice from agents or advisors who promote mark-up loans as beneficial without adequately highlighting associated risks and illegality.

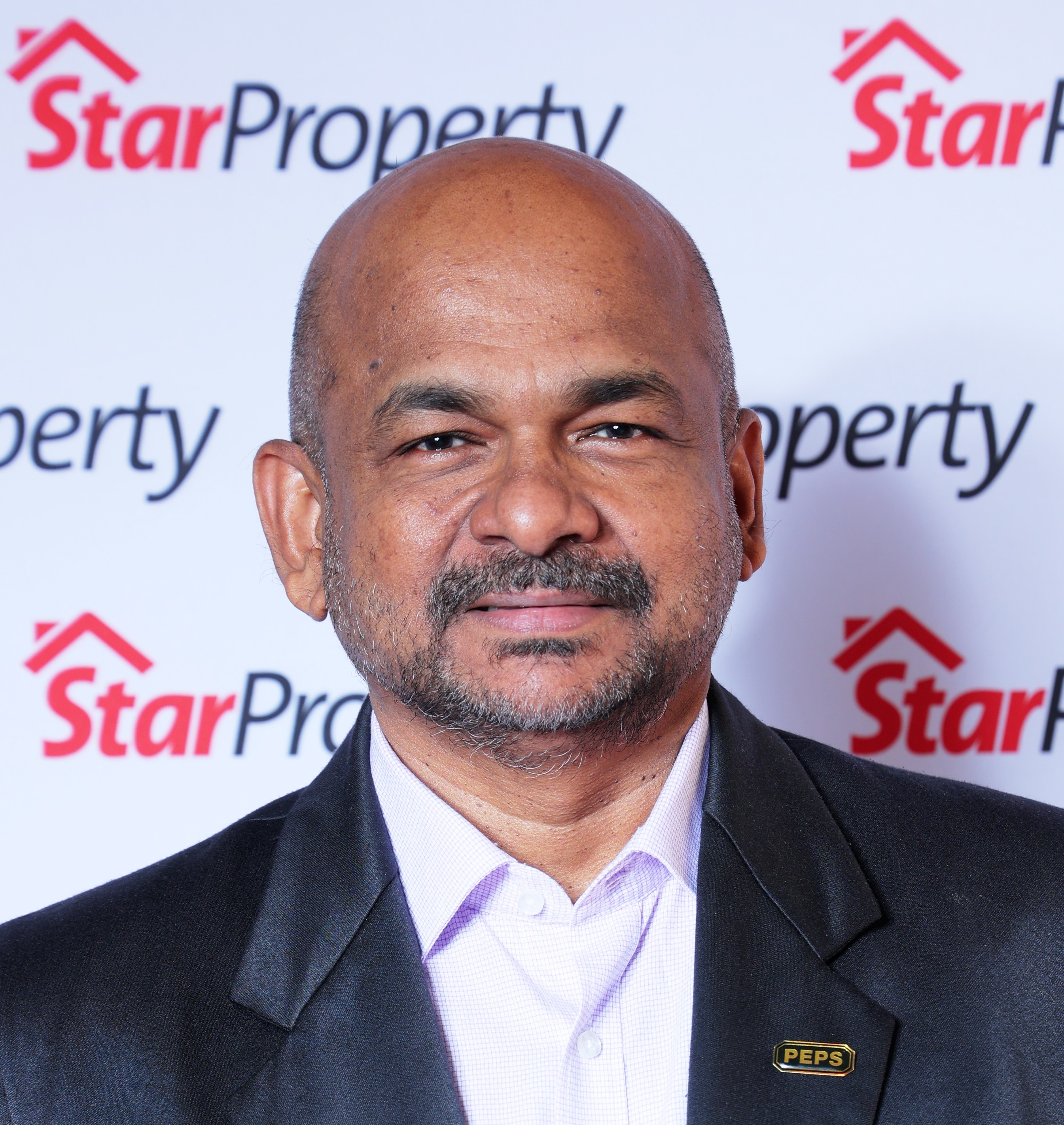

"The valuation profession is highly regulated with practitioners bound by strict standards," said Subramaniam.

Blatantly in the open

Alarmingly, advertisements on popular property listing platforms openly promote mark-up loans and cashback schemes, normalising unethical and illegal practices. Advertisements openly use terms like cashback and mark-up loan, reflecting widespread acceptance. Driven by commissions, some property agents overlook ethical considerations and a minority of valuation professionals might succumb to external pressure or incentives.

Association of Valuers, Property Managers, and Estate Agents in the Private Sector (PEPS) president Subramaniam Arumugam emphasises this issue: “The valuation profession is highly regulated with practitioners bound by strict standards. However, we cannot overlook instances of collusion. Addressing this directly is essential not just for market integrity but also in ensuring market sustainability.”

Thor added: "Beyond using the tools that we've designed to ensure greater compliance to the Malaysian Valuation Standards, we have also developed a platform that is crucial to helping the banks strengthen lending decisions with accuracy, directly from professional valuation practitioners. By enabling greater compliance and mitigating fraud risk before loan disbursement, we can collectively build a more stable and resilient property market in Malaysia."

Tan said this distorts market pricing as it artificially inflates prices, pushing affordability further out of reach for struggling potential home buyers.

The cost of collusion

The impact of mark-up loan fraud is far-reaching, particularly for banks. In the event of a default by a borrower, the bank would be less likely to recover its losses through a sale of the property as the loan amount is larger than the value of the property.

Malaysian Institute of Estate Agents (MIEA) immediate past president Tan Kian Aun opined that the increasing practice of mark up loans and cashbacks especially in the sub sale market “distorts market pricing as it artificially inflates prices, pushing affordability further out of reach for struggling potential home buyers”. Nonetheless, he stressed that “real estate practitioners are reminded that they are bound by strict codes of conduct prohibiting such practices”.

Moreover, the systemic risk to the financial sector is significant. Malaysian banks are increasingly scrutinised by regulators, who stress strict compliance with guidelines such as Bank Negara Malaysia’s Risk Management in Technology (RMiT) and Malaysia’s Personal Data Protection Act (PDPA) 2024. Banks failing to adequately mitigate fraud risk face severe regulatory penalties, reputational damage, and increased scrutiny, necessitating a more robust and transparent valuation process.

“Such fraudulent activities violate banking regulations and ethical standards, constituting financial fraud by misleading lending institutions," said Thor.

Systemic vulnerabilities

The reliance on manual processes and facilitations significantly contribute to mark-up loan vulnerabilities. Traditional processes, characterised by extensive human intervention, create opportunities for errors, influence and intentional manipulation. Manual handling often results in inadequate transparency, limited audit trails and cumbersome compliance monitoring, facilitating fraudulent practices.

The persistence of mark-up loans in Malaysia’s property market highlights urgent systemic vulnerabilities. Proactive action and collaboration across the industry is needed to mitigate fraudulent practices, safeguarding Malaysia’s financial ecosystem and property market integrity.

But despite clear benefits, banks have been slow to adopt digital management systems due multiple reasons. Apart from the perceived high initial investments in digital infrastructure, internal resistance from both management and employees is prevalent as they tend to prioritise immediate returns over strategic long-term advantages, often driven by the push to meet annual Key Performance Indicators (KPIs). Furthermore, the contemporary workforce's inclination to seek new opportunities rather than commit to long-term employment with a single company exacerbates these challenges.

Nevertheless, successfully mitigating mark-up loan fraud requires collective efforts from banks, regulatory bodies, lawyers, property professionals and consumers. This includes enhanced education to inform buyers and industry professionals about the risks and illegality of such schemes. Furthermore, regulatory support is crucial, encouraging banks to adopt technology that promotes greater transparency, thereby reducing the risk of fraud and collusion while enabling better compliance with regulations. Finally, industry collaboration is vital to foster cooperation between valuation professionals, banks and regulators in adopting standardised and transparent digital practices.

Stay ahead of the crowd and enjoy fresh insights on real estate, property development and lifestyle trends when you subscribe to our newsletter and follow us on social media.