CHOOSING the right mortgage insurance may not be a life or death situation, but it is one important life choice. The right insurance might become the life saver for your loved ones when facing the uncertainties of life, while the wrong one will do little to alleviate a difficult financial situation.

CHOOSING the right mortgage insurance may not be a life or death situation, but it is one important life choice. The right insurance might become the life saver for your loved ones when facing the uncertainties of life, while the wrong one will do little to alleviate a difficult financial situation.

In Malaysia, two mortgage life insurance are available to homebuyers – Mortgage Reducing Term Assurance (MRTA) and Mortgage Level Term Assurance (MLTA).

Quoting the “2013 Protection Gap in Malaysia” study, Life Insurance Association of Malaysia (Liam) president Toi See Jong said out of every 10 Malaysians, four to five persons don’t have life insurance.

Such complacency is why most Malaysians are grossly underinsured, and many are risking unsettled loan in the event of accidents or sudden deaths. Thus, transferring the burden of mortgage repayment to the loved ones.

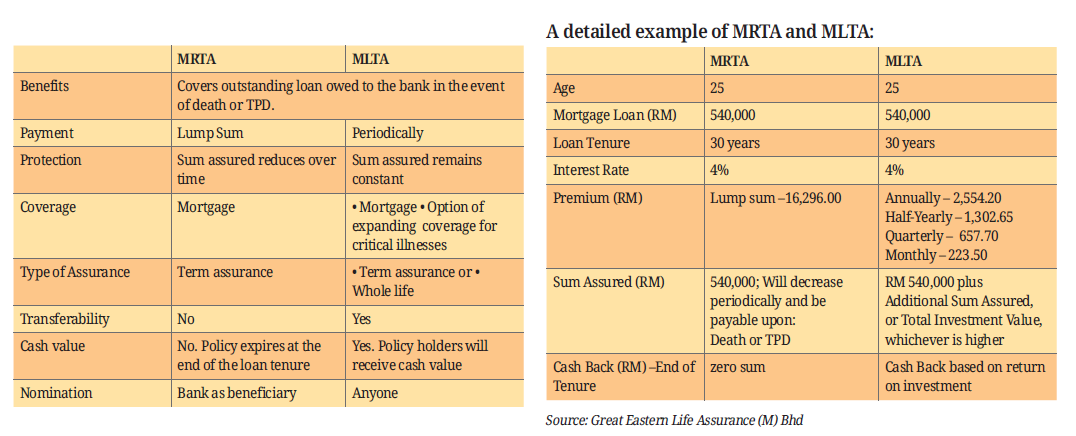

What is the difference between MRTA and MLTA?

As property prices have skyrocketed in recent years, majority of Malaysians find themselves having to utilise the maximal loan-to-value ratio of 90% with longest loan tenure possible to reduce their equated monthly instalment (EMI).

Allianz Life chief executive officer Joseph Gross explained that MRTA and MLTA are commonly pegged to a home loan to cover the loan in the event of the death or TPD of the insured.

“The key difference is MRTA’s sum assured reduces over time while MLTA’s sum assured remains constant throughout the term of the policy,” he said.

Some home loans like flexi home loans allow one to make withdrawals but it will reduce MRTA’s sum over time. When the amount owed to the bank is higher than the MRTA’s sum, the MRTA will not be able to fully cover the home loan.

“While MLTA comes at a higher premium, the flat sum meant the borrower and the family will not have the same concern,” he added.

Mohd Adib Bin Mohd Yazid from Prudential Wealth Planner said since the bank is MRTA's beneficiary, it is unable to protect a borrower’s family in totality.

“MLTA is more personal and often protect your next of kin. If anything happens, the family claims the insurance money. This money can be used to settle the outstanding loan amount since MLTA benefit is fixed sum assured,” he said.

Great Eastern Life Assurance (M) Bhd group agency manager Bon Sze Shean said borrowers should take note that if they decide to cancel MRTA before maturity date, the cash amount that the company will pay you is much less than the total amount premium you have paid.

He added that MLTA is a long-term financial commitment. It is not advisable to hold this plan for a short period of time in view of the high initial costs.

“If you find the fund that you have chosen is no longer appropriate, you have the flexibility to switch fund,” he added.

Bon also opined that borrowers should avoid surrendering their MLTA because if designed properly, the cash value can break even.

“Treat it as savings and use the cash value to pay off your loan (early settlement) in the later years and save on interest,” he said.

When asked if MRTAs and MLTAs are absolutely necessary, Jared Lim Loanstreet co-founder suggested that borrowers weigh their risks holistically from an estate planning perspective.

“If you are sufficiently covered by a life insurance policy, you can even consider skipping the MRTA or MLTA. But note that your beneficiaries will get lesser if you lose your ability to generate income,” Lim said.

He added that borrowers must go through the trouble of making sure their next of kin is aware of their policy and know how to make claims.

Adib said the process of insurance claim is basically the same for MRTA or MLTA. In the event of death, the claimant would need supporting documents such as certified copy of death certificate, copy of deceased identification card, burial permit, medical report, identity of claimant, proof of claimant relationship with deceased and most importantly, the original policy document.

“It is highly important to educate your family on this subject matter,” he said.

Read More:

MRTAs & MLTAs – What are they, and do you need it?

Useful tips on property and more

Q&A: For MRTAs, do I need to get a Malaysian policy or can I get a cheaper Singaporean one?

Mortgage Reducing Term Assurance (MRTA): Why would you need it?